Beyond Zero-Based Budgeting

How to choose a budgeting system you will actually keep using, with figures, comparison table, and references.

Educational content. Not financial, legal, or tax advice. Examples are illustrative; confirm your numbers and consult licensed professionals for personalized advice.

Quick links

- Start your free trial (PYB)

- Budget Tool (account access)

- Downloads hub

- Budget Reset Workbook (PYB download)

- Zero-Based Budget Template (PYB download)

- Debt Payoff Planner (PYB)

Executive summary

Summary: Zero-based budgeting is effective because it gives every dollar a job, but it is not the only sound way to manage money. Simpler frameworks such as 50/30/20, pay-yourself-first, and envelope budgeting can be easier to maintain, especially for households dealing with variable income, busy schedules, or budget fatigue. This article compares the main alternatives, shows where each one fits, and offers a practical path for choosing the right system.

Why this question matters

Many people first encounter budgeting through the zero-based method: list your take-home pay, assign every dollar to a category, and make the month balance to zero once bills, savings, debt payments, and discretionary spending have all been planned. That approach is powerful because it forces intention. Fidelity describes zero-based budgeting as a framework in which every dollar of take-home pay is assigned a job, with the goal of making income minus outflows equal zero by the end of the month.[3]

PYB implementation note: If you want to apply any of the methods in this article without building a system from scratch, PayYerBills (PYB) pairs a free trial of budgeting tools with a download center of templates and checklists. Start with the Download Center, then connect your budget to a payoff plan when you’re ready.

The problem is not that zero-based budgeting is wrong. The problem is that a budgeting system can be technically correct and still fail in real life. A parent with rotating childcare costs, a household with irregular freelance income, or a worker who simply hates category micromanagement may abandon a zero-based budget not because the math is bad, but because the maintenance cost is too high. In other words, the best budget is not always the one with the most detail. It is the one a person will still be using six months from now.[1][3]

Official consumer guidance starts from the same foundation. Consumer.gov defines a budget as a written plan for deciding how money will be spent each month, and its step-by-step advice begins with gathering bills and pay stubs, listing expenses, estimating income, and checking whether spending stays below income.[1] That definition is broad on purpose: a budget is a plan, not a single branded formula.

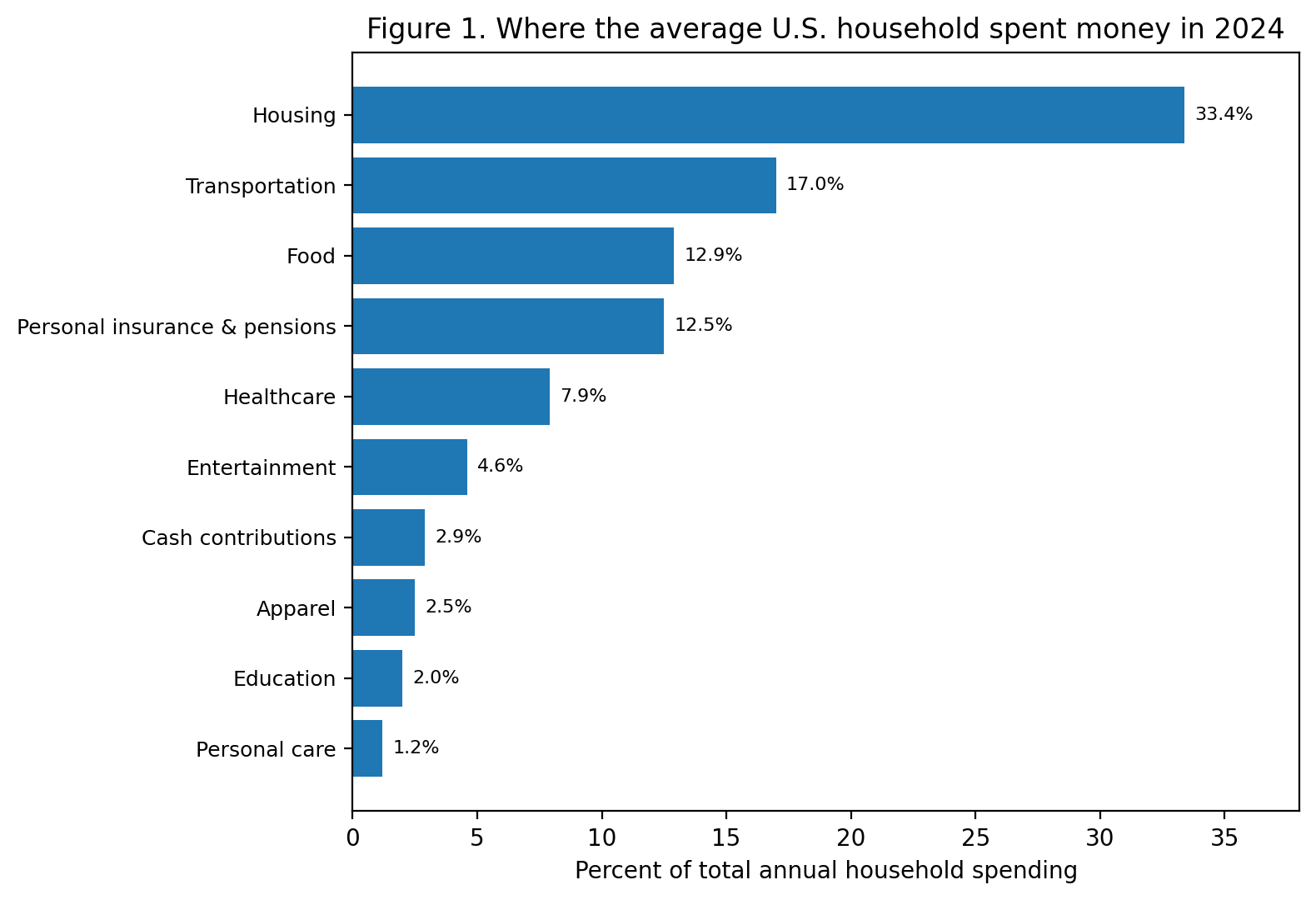

Figure 1. BLS data show why budgeting systems usually begin with housing, transportation, food, and savings capacity. Source: adapted from U.S. Bureau of Labor Statistics 2024 consumer expenditure data.[7]

Figure 1. BLS data show why budgeting systems usually begin with housing, transportation, food, and savings capacity. Source: adapted from U.S. Bureau of Labor Statistics 2024 consumer expenditure data.[7]

The need for flexibility becomes clearer when current spending patterns are considered. According to the U.S. Bureau of Labor Statistics, average annual household spending in 2024 was $78,535, with housing alone consuming 33.4% of total spending and transportation another 17.0%. Food represented 12.9%, and personal insurance and pensions 12.5%.[7] When so much of a household budget is absorbed by large fixed or semi-fixed categories, a budgeting system must do more than create discipline; it must also fit actual cash-flow pressure.

What zero-based budgeting does well

Zero-based budgeting remains popular for good reasons. First, it creates visibility. Instead of treating savings as something that happens with leftover money, it makes saving, debt payoff, and bills part of the plan up front.[3] Second, it surfaces tradeoffs quickly. Because there is no unassigned money, every additional dollar to dining out, shopping, or subscriptions must come from somewhere else. Third, it can be customized month to month, which makes it useful during periods of financial change such as a move, a new job, or an aggressive debt payoff season.[3]

But the same strengths can become weaknesses. A detailed system demands active maintenance, advance planning, and frequent recategorization. Fidelity notes that zero-based budgeting requires planning ahead and can be more difficult for people with inconsistent incomes.[3] That point is crucial. The tighter the system, the more fragile it can become when life becomes unpredictable.

Practical takeaway: zero-based budgeting is often best for people who want maximum control, are comfortable reviewing money weekly, and benefit from seeing exactly where every dollar goes.

PYB quick-start: If you want a ready-made worksheet plus a weekly check-in routine to operationalize zero-based budgeting, download the PYB Zero-Based Budget Template package.

Five strong alternatives to zero-based budgeting

Once budgeting is framed as a design choice rather than a single ideology, several alternatives stand out. Each solves a different problem: some reduce friction, some increase awareness, and some push savings or debt reduction ahead of everything else.[1][4][5][6]

Table 1. Comparison of common alternatives to zero-based budgeting. Method descriptions synthesized from consumer guidance and financial education sources.[1][4][5][6]

| Method | Best for | Control | Effort | Main tradeoff |

|---|---|---|---|---|

| 50/30/20 | Beginners who want a fast framework | Medium | Low | Can feel too generic in expensive areas |

| Pay yourself first | Saving or debt payoff as the main goal | Low-Med | Very low | Less visibility on smaller spending leaks |

| Envelope system | Impulse spending in a few categories | High | Medium | Less convenient in a cashless world |

| Essentials-first | Tight or variable income | Medium | Low | Not as useful for fine-grained optimization |

| Hybrid percentage budget | People who want structure without micromanagement | Medium-High | Low-Med | Needs occasional recalibration |

1. The 50/30/20 budget

The 50/30/20 system is arguably the best-known alternative because it offers a fast mental model. NerdWallet summarizes it as 50% of take-home pay for needs, 30% for wants, and 20% for savings and debt repayment.[4] Its strength is that it gives a person boundaries without forcing them to account for every dollar. Someone can check broad ratios once or twice a month and still keep the plan intact.

This method works especially well for beginners, dual-income households with relatively stable pay, and anyone who freezes when a budget becomes too detailed. It is also useful as a diagnostic tool: if needs alone are far above 50%, the problem may not be coffee or streaming subscriptions at all, but housing costs, transportation, insurance, or debt burden.[4][7]

The main weakness is that 50/30/20 can feel unrealistic in high-cost environments. A household dealing with expensive rent, childcare, or medical costs may exceed the suggested 'needs' share before wants are even considered. That does not make the method useless; it simply means the percentages should be treated as a guide rather than a rigid scorecard.[4]

2. Pay yourself first

The pay-yourself-first method flips the usual order of operations. Instead of budgeting every expense in advance, the household decides what amount will go to savings, investing, or extra debt payments first, then lives on the rest. NerdWallet describes reverse budgeting as putting savings aside first and then allocating the remaining money across needs and wants, with the percentages adjustable rather than fixed.[5]

This system is excellent for people whose main issue is not financial ignorance but financial drift. They know they should save; they simply do not do it consistently. The Consumer Financial Protection Bureau recommends automating savings because regular small transfers are one of the easiest and most consistent ways to build the habit. The agency also notes that automatic transfers can effectively help a person pay themselves first before other expenses absorb the money.[2]

Research on savings behavior helps explain why this approach can work. A 2022 NBER study reviewing behavioral interventions found that information, simplification, active choice, and automatic enrollment all increase retirement savings, with stronger interventions producing larger effects.[8] For ordinary households, the practical lesson is simple: automation can compensate for weak willpower. A budget that runs partly on defaults will often outperform a perfect budget that depends on daily self-control.[2][8]

3. The envelope or cash-stuffing system

Envelope budgeting is less about total planning and more about category control. Fidelity describes cash stuffing as a system that separates money into envelopes for planned expenses and then uses that cash as spending occurs, with the explicit goal of making spending more mindful.[6] In effect, the method places a physical boundary around categories that tend to leak money, such as groceries, dining out, entertainment, or miscellaneous shopping.

The envelope system is particularly effective when a person does not overspend everywhere, but consistently overspends in a few volatile categories. In that case, a full zero-based budget may be more machinery than necessary. A hybrid approach often works better: automate bills and savings, then use envelopes only for the categories that repeatedly cause trouble.[2][6]

Its disadvantages are mostly practical. Cash is less convenient, some expenses are now digital by default, and not all household members enjoy handling categories this way. But the underlying principle remains powerful even in digital form: give problem categories a hard ceiling instead of hoping awareness alone will fix them.[6]

4. Essentials-first or priority budgeting

An essentials-first budget is not always marketed with a catchy label, but it is one of the most useful systems in the real world. Consumer.gov's budgeting steps begin with listing bills and expenses, estimating income, and checking whether the result is above zero.[1] For households under pressure, that logic can be turned into a triage model: cover housing, utilities, food, insurance, transportation to work, minimum debt payments, and required childcare first; then assign anything left to savings, extra debt, or discretionary spending.

This approach is especially appropriate for variable income, temporary hardship, or high uncertainty. Consumer.gov specifically advises people who are not paid monthly to estimate monthly income using last year's income divided by twelve.[1] That recommendation naturally supports a conservative version of budgeting: build the plan around a low or average month, not an optimistic one.

Essentials-first budgeting does not produce the same feeling of optimization as a detailed zero-based system, but during unstable periods optimization is not the point. Stability is the point. A budget is serving its purpose if the most important bills are paid on time and cash shortfalls are less frequent.

5. Hybrid percentage budgeting

A hybrid percentage budget sits between strict category planning and loose guideline budgeting. Rather than using 50/30/20 exactly, a household creates custom bands that match reality—for example, 60% essentials, 15% long-term savings, 10% extra debt payoff, 10% flexible spending, and 5% sinking funds. Fidelity notes that other strategies, such as its 60/30/10 guideline, provide broad percentages for essentials, extras, and near-term goals while also encouraging retirement saving.[3]

This style is often the best compromise for people who want structure but dislike the maintenance burden of zero-based budgeting. It preserves accountability at the level that matters—how much total income is going to essentials, future goals, and discretionary consumption—without forcing a person to assign every last dollar on day one.[3][4]

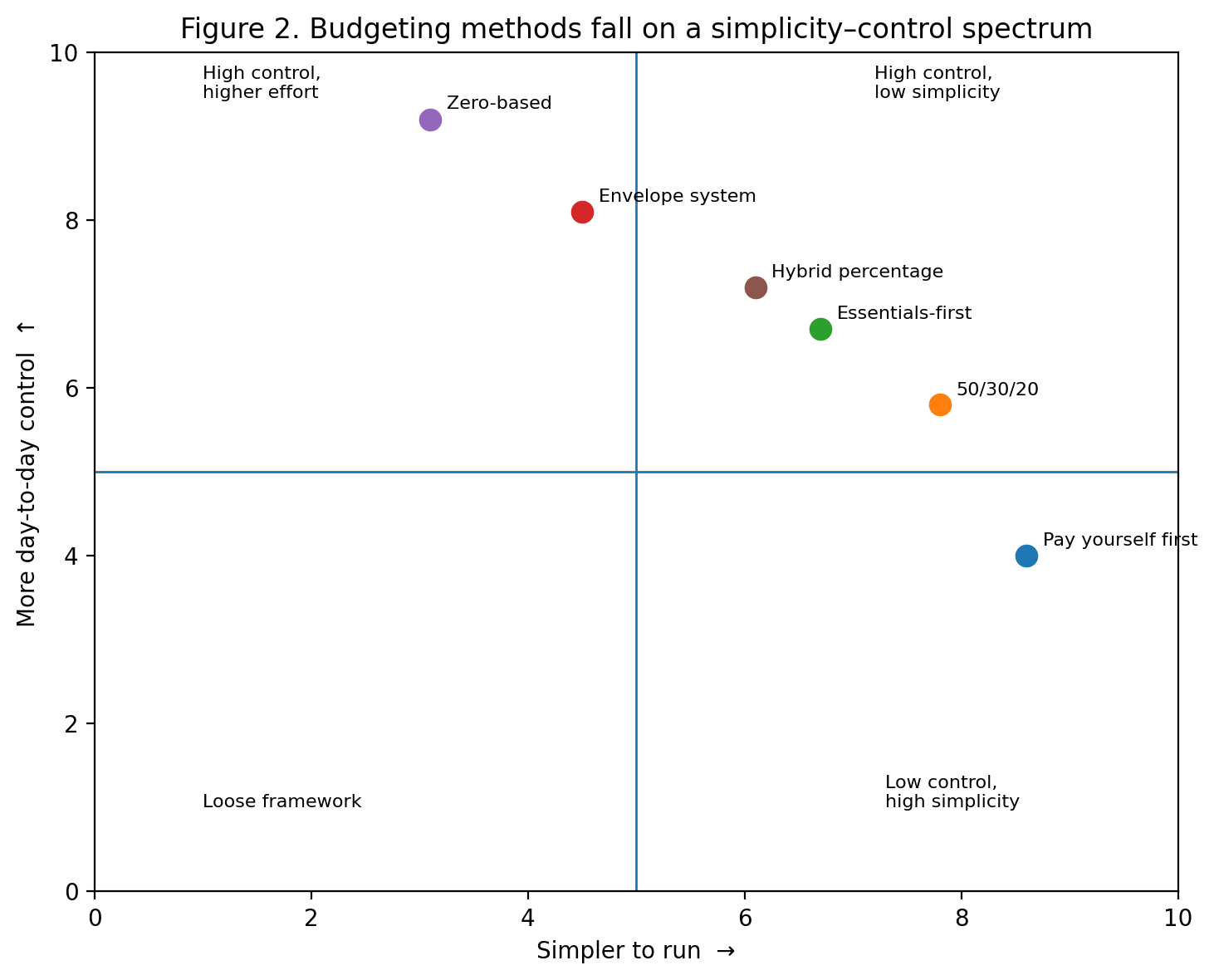

Figure 2. Author synthesis showing where common methods tend to land on the simplicity–control spectrum based on the cited descriptions of each system.[1][3][4][5][6]

Figure 2. Author synthesis showing where common methods tend to land on the simplicity–control spectrum based on the cited descriptions of each system.[1][3][4][5][6]

Matching the budget to the person

One reason budget advice often feels contradictory is that people are trying to solve different problems with the same tool. A person living paycheck to paycheck, a high earner with impulse spending, and a disciplined saver trying to optimize long-term investing do not need the same kind of budget. Good financial planning starts by diagnosing the friction point.

Use zero-based budgeting when the core issue is lack of visibility and you need to see precisely where money is going.

Use 50/30/20 when you want a fast, low-friction framework and your income is relatively stable.

Use pay-yourself-first when the real goal is consistent saving or debt acceleration, not category perfection.

Use envelope budgeting when overspending is concentrated in a few discretionary categories.

Use essentials-first when income is variable, cash is tight, or financial stability matters more than optimization.

Use a hybrid percentage system when you want guardrails but not micromanagement.

There is also no rule requiring loyalty to a single system forever. A household can use essentials-first budgeting during a job transition, move into pay-yourself-first once income stabilizes, and eventually graduate to a hybrid percentage budget or detailed zero-based system. Budgeting methods are tools, not identities.

How automation changes the budgeting conversation

Automation deserves separate attention because it can make almost any budgeting style more durable. The CFPB explains that one of the easiest ways to save is to set recurring transfers from checking to savings, often timed around payday.[2] That advice applies far beyond savings. Automatic bill pay, scheduled debt payments, and recurring transfers to sinking-fund accounts reduce the number of financial decisions that have to be made manually each month.

PYB note: If you want automation + tracking in one place (bills, due dates, and payoff plan staying in sync), the PYB Budget Tool dashboard keeps your workflow connected.

The significance of automation is behavioral, not just administrative. The NBER literature shows that more forceful savings interventions—especially defaults and automatic enrollment—can materially raise participation and contributions.[8] While household budgeting is not the same as employer retirement-plan design, the principle translates cleanly: the less a person must rely on memory, motivation, and repeated decision-making, the more likely the plan is to survive ordinary life.

This is why a so-called 'looser' budget can outperform a tighter one. A reverse budget with automated savings and bill pay may look less sophisticated on paper than a 25-category zero-based worksheet, but if the automated version consistently produces savings and on-time payments, it is the better system for that household.[2][5][8]

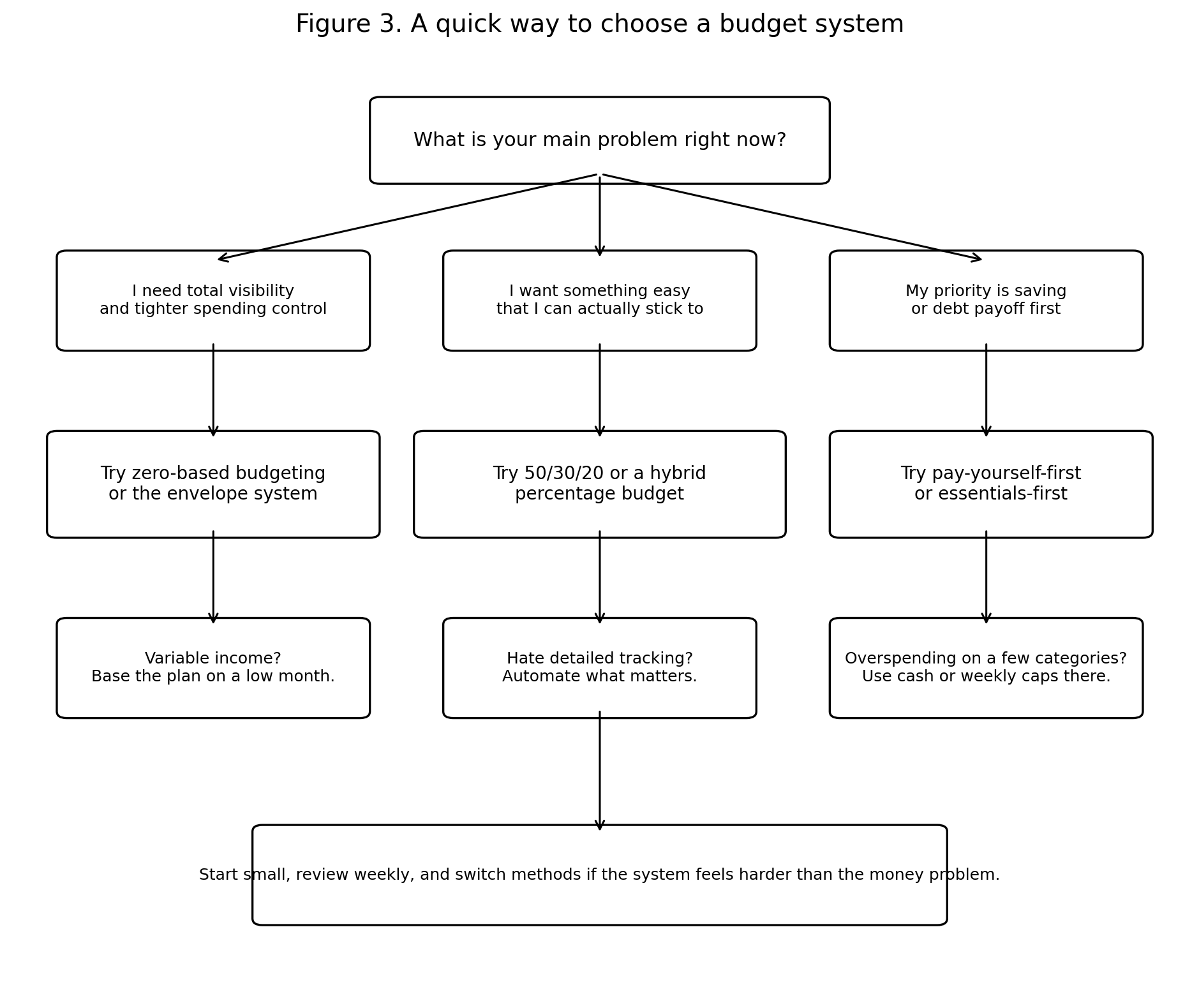

Figure 3. Decision aid for selecting a budgeting style. This flowchart is an author-created synthesis grounded in the goals and constraints described across the cited budgeting sources.[1][2][3][4][5][6]

Figure 3. Decision aid for selecting a budgeting style. This flowchart is an author-created synthesis grounded in the goals and constraints described across the cited budgeting sources.[1][2][3][4][5][6]

A 30-day way to test a new budgeting approach

A useful budgeting experiment should be short enough to survive the awkward first month. The following 30-day process is intentionally simple and can be adapted to any method.

PYB shortcut: If you want a faster start than a full 30-day experiment, run PYB’s 20-minute cash-flow reset guide first, then choose your budgeting method with cleaner numbers.

Week 1: Pull one to three months of bank and card activity, list fixed bills, and estimate average take-home income.[1][4]

Week 1: Decide what problem you are solving first: overspending, no savings, chaotic cash flow, debt acceleration, or poor visibility.

Week 2: Choose one primary system. Pair it with automation wherever possible, especially for savings and fixed bills.[2]

Week 2: Create only the categories that matter. Avoid a long list unless you are intentionally using a detailed zero-based approach.

Week 3: Review one time mid-month. Do not constantly rebuild the entire plan unless income changes materially.

Week 4: Ask whether the system reduced stress, improved savings, or prevented overspending. If not, simplify or switch.

The test matters because adherence is easier to evaluate than theoretical elegance. A person does not need to ask, 'What is the best budget in the abstract?' They need to ask, 'What plan made me more likely to pay bills, save, and stay consistent this month?'

Common mistakes when people move away from zero-based budgeting

The first mistake is replacing a detailed budget with no budget at all. Simpler methods still require a plan, a savings target, and periodic review.[1][2][4] The second mistake is keeping too many categories even after choosing a simpler system. The point of 50/30/20 or pay-yourself-first is to reduce maintenance, not merely relabel the same complexity.

A third mistake is ignoring irregular expenses. Annual insurance premiums, holidays, car repairs, school costs, and medical bills can destroy an otherwise reasonable budget if they are treated as surprises. Even simple systems need sinking funds or periodic reserves. A fourth mistake is selecting a method based on identity rather than circumstance. People sometimes cling to a budgeting style because it feels disciplined, minimalist, or fashionable. The better question is whether it fits current income, obligations, and behavior.

Finally, many households underestimate how emotionally important a budgeting method feels. Some people need the reassurance of knowing where every dollar is going. Others need a system that feels light enough to avoid burnout. Personal fit is not a weakness in a budgeting strategy; it is one of the main determinants of whether the strategy will last.

Conclusion

There is absolutely a different approach to budgeting than zero-based budgeting—several, in fact—and many people will do better with one of them. The strongest alternatives are not random shortcuts. They represent different tradeoffs between control, flexibility, and effort. 50/30/20 offers quick structure. Pay-yourself-first builds savings through prioritization and automation. Envelope budgeting adds hard limits to weak spots. Essentials-first budgeting protects stability during uncertainty. Hybrid percentage budgets create structure without daily micromanagement.[1][2][3][4][5][6]

A budget is working when it reliably helps a household spend below income, pay important bills on time, and move money toward goals. Once that standard is accepted, the debate changes. The question is no longer whether zero-based budgeting is the best method in theory. The better question is which method makes good decisions easiest in practice.

Want to put the method you chose into action? Start with PYB’s Budget Reset Workbook (a four-step cash-flow reset), the Zero-Based Budget Template starter kit, and the PYB Download Center.

References

[1] Consumer.gov. “Making a Budget.” Federal Trade Commission.

[2] Consumer Financial Protection Bureau. “Looking for an easy way to save money? Make it automatic.” August 26, 2019.

[3] Fidelity. “What is zero-based budgeting and how does it work?”

[4] NerdWallet. “50/30/20 Budget Calculator.”

[5] NerdWallet. “What Does Pay Yourself First Mean? Reverse Budgeting Explained.” Updated September 24, 2025.

[6] Fidelity. “What is cash stuffing? Cash envelope system explained.”

[7] U.S. Bureau of Labor Statistics. “Housing and transportation accounted for 50 percent of household spending in 2024.” The Economics Daily, February 12, 2026.

[8] Patterson, Richard W., et al. “How do Behavioral Approaches to Increase Savings Compare? Evidence from Multiple Interventions in the U.S. Army.” NBER Working Paper 30697, 2022.

[9] Consumer Financial Protection Bureau. “Creating a cash flow budget” (tool PDF).

[10] Consumer Financial Protection Bureau. “Monthly budget” (tool PDF).

[11] PayYerBills (PYB). Templates & Downloads hub.

[12] PayYerBills (PYB). Budget reset workbook download.

[13] PayYerBills (PYB). Zero-based budget template download.

[14] PayYerBills (PYB). Budget tool dashboard (account access).

[15] PayYerBills (PYB). Debt payoff planner.