Should You Pay Off Your Mortgage Early? The Decision Framework (with Real Math)

A professional guide to extra principal, invest-vs-prepay tradeoffs, refinance break-even, and a step-by-step walkthrough inside PYB’s Mortgage Amortization Intelligence tool.

Educational content. Not financial, legal, or tax advice. Examples are illustrative; confirm terms with your lender/servicer and consult licensed professionals for personalized advice.

Quick links

- Mortgage Amortization Intelligence (PYB)

- Budget Reset Workbook (PYB download)

- Debt Payoff Planner (PYB)

- Budget Tool (account access)

- Downloads hub

Executive summary: the honest answer

“Pay off your mortgage early” is one of the most debated money moves because it mixes two different questions:

- What is the best expected math outcome?

- What is the best real-life outcome for a household that is busy, risk-averse, and not running a hedge fund?

Many advisors caution against rushing to prepay a low-rate mortgage because the money might earn more invested over long horizons, and because mortgage prepayment can reduce liquidity. Publications and firms often frame this as an “overpay vs invest” comparison. [8][9][10]

But that argument only wins if you actually invest the difference consistently for years and can tolerate volatility.

The simplest professional way to decide is to treat mortgage prepayment as a guaranteed, risk-free return equal to your interest rate (after tax considerations), then compare it to your realistic, after-tax, risk-adjusted alternative returns and your behavior. Vanguard describes this as a household balance-sheet allocation problem: which cash-flow choice best maximizes after-tax net worth while still meeting near-term stability needs. [11]

- If your mortgage rate is high (or you hate risk), paying extra can be a very strong “guaranteed return.”

- If your mortgage rate is low and you truly invest the difference for the long term, investing can win—often by a lot—depending on returns.

- If you’re not consistently investing the difference, the invest-vs-prepay math is irrelevant; extra principal can become a built-in discipline tool.

- Before either move: stabilize cash flow and eliminate high-APR consumer debt first.

The PYB decision framework (5 checkpoints)

Checkpoint 1: Do you have high-APR consumer debt?

If you have credit cards at high APRs, they usually dominate this decision. A 20%+ revolving APR is a different universe than most mortgages. Treat it as a priority payoff item before accelerating a 3%–7% mortgage.

Use Debt Payoff Planner (PYB) to quantify this first.

Checkpoint 2: Is your emergency buffer strong enough to avoid new debt?

This is where “advisors say don’t pay it off” can be correct: you can’t eat home equity. If prepaying leaves you cash-tight, one unexpected expense can force you back into high-APR debt—and that defeats the whole point.

Make the payoff plan durable first (budget reset + buffer). Start with Budget Reset Workbook (PYB download) to rebuild your baseline budget and protect your buffer.

Checkpoint 3: Are you capturing employer retirement match (if available)?

A match can be an immediate, high “return” that can beat mortgage prepayment. (Exact details vary by plan and eligibility.) If you’re leaving match dollars on the table, fix that before optimizing mortgage acceleration.

Checkpoint 4: What is your mortgage rate “as a guaranteed return”?

If you prepay principal, you reduce the balance on which interest accrues. That creates a guaranteed return equal to your mortgage rate on the prepaid amount (ignoring taxes/PMI and any prepayment penalties).

If your rate is 6.5%, prepaying principal is roughly like earning a risk-free 6.5% return on that money.

Rate context matters. Freddie Mac’s Primary Mortgage Market Survey (PMMS) publishes weekly average mortgage rates; FRED also tracks the 30-year fixed series (MORTGAGE30US). [6][7] PYB’s Mortgage Amortization Intelligence can use this context while comparing scenarios. [12]

Checkpoint 5: Behavior check — will you actually invest the difference?

This is the part most calculators skip. The invest-instead argument assumes that if you don’t prepay the mortgage, you invest the exact same dollars, month after month, through good markets and bad.

Many households don’t do that.

- If you will invest automatically and can stay invested through volatility: compare expected after-tax returns vs your mortgage rate.

- If you won’t invest reliably: prepaying can be the better real-life move even if spreadsheets say otherwise.

- If you want a hybrid: split the difference (for example, 50% extra principal and 50% investing) and automate both.

Mortgage amortization: why extra principal works

A mortgage payment is split between interest and principal. Early in the loan, interest is a larger share because the balance is large. As principal declines, interest declines, and more of the payment goes to principal. The CFPB explains this amortization dynamic: early payments are more interest-heavy, later payments shift toward principal. [1]

Extra principal attacks the balance directly. A smaller balance produces less interest next month. That accelerates principal reduction, and the cycle compounds.

Real math example (illustrative)

Scenario used for illustration:

- Principal: $350,000

- Term: 30 years

- APR: 6.5%

- Monthly payments

- No PMI

- No prepayment penalty assumed

Baseline principal-and-interest payment (approx.): $2,212.24 per month.

Payoff timeline and interest savings at different extra-payment levels

| Extra payment | Payoff (months) | Payoff (years) | Total interest ($) |

|---|---|---|---|

| $0/mo | 360 | 30.0 | 446405.71 |

| $100/mo | 318 | 26.5 | 383778.66 |

| $250/mo | 273 | 22.75 | 319801.73 |

| $500/mo | 223 | 18.58 | 252803.19 |

| $1,000/mo | 166 | 13.83 | 180451.66 |

In this example, adding $500/month cuts payoff time from 30 years to about 18.6 years and reduces total interest by roughly $193,603.

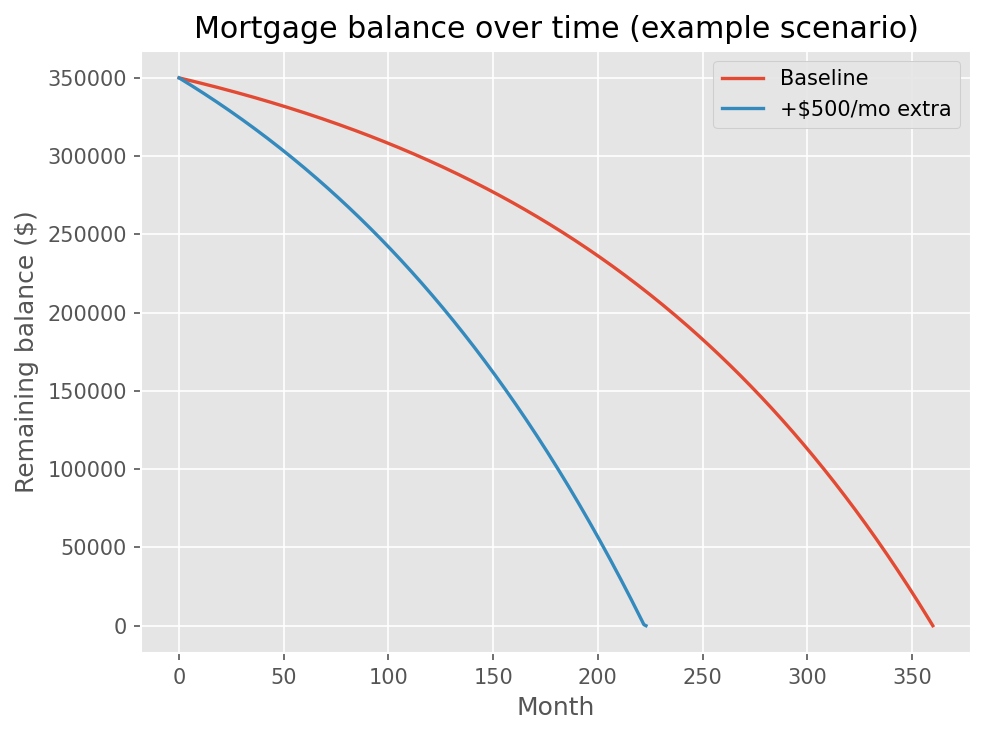

Balance path visualization

With the same loan, adding extra principal each month drives the remaining balance down much faster than making the baseline payment alone.

Figure: Remaining balance over time for baseline vs +$500/month extra (illustration).

Biweekly payments: what actually drives results

Biweekly plans are often marketed as a “hack.” The mechanism is simple: paying half the monthly payment every two weeks produces 26 half-payments per year (equivalent to 13 full monthly payments).

The CFPB describes this structure and notes borrowers should review terms for possible prepayment penalties. [2]

If your servicer supports a true biweekly schedule without fees, it can be clean and effective. You can often replicate most of the effect by adding about one extra monthly payment per year, spread across the year.

The key is that extra amounts are applied to principal.

Invest vs prepay: professional framing

Mortgage prepayment is a guaranteed return equal to your mortgage rate. Investing is an uncertain return with volatility and potentially higher expected long-run returns.

This is not purely a math question. It is math + risk + behavior + liquidity. Vanguard frames it as optimizing after-tax net worth while meeting short-term household needs. [11]

You do not need a lump sum for investing to matter

The invest-instead approach can be monthly. Monthly investing compounds too.

But returns are not guaranteed. Historical equity returns vary significantly year to year; Damodaran’s long-run data shows broad variability over time. [13]

Scenario comparison with the same $500/month cash flow

To compare fairly over the same 30-year horizon:

- Strategy A: Pay normal mortgage, invest $500/month from month 1.

- Strategy B: Pay $500/month extra into mortgage until payoff, then invest former mortgage payment + $500/month for remaining months.

| Assumed annual return | Payoff month with +$500 | Invest extra from day 1 (A) FV | Pay extra then invest after payoff (B) FV | A - B ($) |

|---|---|---|---|---|

| 4% | 223 | 342635.28 | 467942.54 | -125307.25 |

| 7% | 223 | 584726.3 | 558855.56 | 25870.74 |

| 10% | 223 | 1031421.66 | 669612.79 | 361808.87 |

Interpretation:

- At lower assumptions (for example, 4%), prepaying then investing later can win.

- At higher assumptions (for example, 10%), investing from day 1 can win by a lot because compounding starts earlier.

- Around mid-range assumptions (for example, 7%), outcomes can be close, making behavior and risk tolerance decisive.

Why “don’t rush to pay it off” can be right—and wrong

The typical advisor case against aggressive prepayment is:

- preserve liquidity,

- invest for long-term growth,

- avoid locking too much cash into home equity.

Vanguard and Morningstar discuss these tradeoffs and note that higher mortgage rates strengthen the case for prepayment. [8][10]

That guidance breaks for many real households when the “invest the difference” step doesn’t happen consistently.

- If the difference is spent (not invested), it is not an invest-vs-prepay comparison anymore.

- If debt stress is high and lower fixed obligations improve resilience, prepayment can still be rational.

- If the mortgage rate is high, guaranteed savings from prepayment become more compelling.

Refinance vs extra payments: break-even math

Refinancing can lower your rate or change term, but usually includes closing costs. The CFPB summarizes common closing costs and who pays them. [3]

Basic break-even test:

Break-even months = total closing costs ÷ monthly payment savings

Points vs lender credits changes break-even. The CFPB explains this tradeoff: points reduce rate with more cash up front, while lender credits reduce upfront cost in exchange for a higher rate. [4]

- If you expect to keep the loan beyond break-even, refinancing may be worth modeling.

- If your horizon is uncertain, extra principal can be a cleaner acceleration path.

Implementation pitfalls that break payoff plans

1) Extra payments not applied to principal

The CFPB warns that if extra payments are allowed, borrowers should confirm they are applied to principal rather than interest. [5]

2) Prepayment penalty or overpayment limits

Some mortgages include prepayment penalties or limits. Review your note and disclosures. [14]

3) Cash-flow fragility

Paying extra while underfunded on cash reserves often leads to borrowing on high-APR debt during shocks.

How to model this in PYB

Use Mortgage Amortization Intelligence (PYB) to compare baseline, extra-payment, lump-sum, and refinance scenarios side-by-side.

Suggested workflow:

- Enter your real loan amount, term, APR, and start date.

- Build Scenario A = baseline.

- Build Scenario B = monthly extra (test $100/$250/$500).

- Build Scenario C = refinance case (APR, term, closing costs) if relevant.

- Compare payoff dates, lifetime interest, and year-1 interest.

- Export PDF/CSV for partner or lender review.

Execution plan: make payoff durable

The biggest failure point is usually cash-flow fragility, not amortization math.

- Reset baseline budget with the Budget Reset Workbook.

- Track your monthly execution in Budget Tool (account access).

- If high-APR debt exists, clear that first with Debt Payoff Planner.

- Run side-by-side mortgage scenarios in Mortgage Amortization Intelligence.

- Keep templates and exports organized in the Downloads hub.

Optional but useful: maintain a balance-over-time chart and a total-interest bar comparison to keep tradeoffs visible during quarterly reviews.

Bottom line

Paying off a mortgage early can be brilliant or unnecessary depending on rate, liquidity, and behavior.

The professional move is to stop treating this like a belief system and run it as a scenario decision: use real numbers, compare realistic alternatives, and choose the plan you will actually execute for years.

References

Citations in the text appear as [#]. URLs are included for editor verification.

- CFPB. How does paying down a mortgage work? https://www.consumerfinance.gov/ask-cfpb/how-does-paying-down-a-mortgage-work-en-1943/

- CFPB. Mortgages key terms (bi-weekly payment explanation and principal application notes). https://www.consumerfinance.gov/language/cfpb-in-english/mortgages-key-terms/

- CFPB. What fees or charges are paid when closing on a mortgage? https://www.consumerfinance.gov/ask-cfpb/what-fees-or-charges-are-paid-when-closing-on-a-mortgage-and-who-pays-them-en-1845/

- CFPB. How should I use lender credits and points (discount points)? https://www.consumerfinance.gov/ask-cfpb/how-should-i-use-lender-credits-and-points-also-called-discount-points-en-136/

- CFPB. Your mortgage servicer must comply with federal rules (extra payments applied to principal). https://www.consumerfinance.gov/consumer-tools/mortgages/your-mortgage-servicer-must-comply-with-federal-rules/

- Freddie Mac. Primary Mortgage Market Survey (PMMS). https://www.freddiemac.com/pmms

- FRED. 30-Year Fixed Rate Mortgage Average in the United States (MORTGAGE30US). https://fred.stlouisfed.org/series/MORTGAGE30US

- Vanguard Investor (UK). Should I overpay my mortgage or invest? https://www.vanguardinvestor.co.uk/articles/latest-thoughts/investing-success/should-i-overpay-my-mortgage-or-invest

- Vanguard Professional. Investing or paying off debt? A framework. https://www.nl.vanguard/professional/vanguard-365/investing-or-paying-off-debt-a-framework

- Morningstar. Pay Down Mortgage or Invest? (2024 edition). https://www.morningstar.com/personal-finance/pay-down-mortgage-or-invest-2024-edition

- Vanguard (PDF). What to do with your next dollar: A quantitative framework. https://corporate.vanguard.com/content/dam/corp/research/pdf/what_to_do_with_your_next_dollar.pdf

- PayYerBills. Mortgage Amortization Intelligence tool page (includes FRED benchmark context). https://www.payyerbills.com/tools/mortgage-amortization

- NYU Stern (Damodaran). Historical Returns on Stocks, Bonds and Bills (includes S&P 500 total returns by year). https://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html

- CFPB. What is a prepayment penalty? https://www.consumerfinance.gov/ask-cfpb/what-is-a-prepayment-penalty-en-1957/